The documenting of internal controls

|

Just as Grant Thornton believed that the accounting profession should accept a principles-based versus rules-based approach to accounting, the firm also believed that they should take a principles-based approach in adhering to the Sarbanes-Oxley legislation. Although some areas in the legislation are clear, other areas are capable of interpretation. Grant Thornton believed that the guide in gray areas should be the spirit of reform and protection of investors that the bill’s authors intended. The firm firmly believed that it was wrong for any auditor to audit their own work.

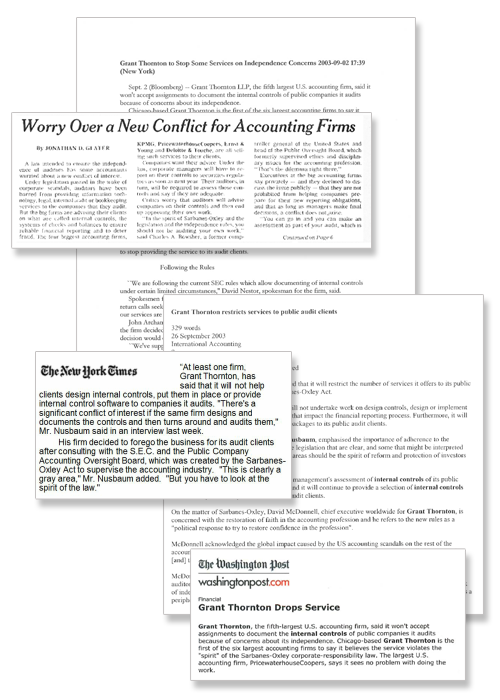

For this reason, in 2003, Grant Thornton refused to accept engagements to document our public audit clients’ internal controls (including documenting existing controls), or perform evaluations of existing controls that management uses to support their conclusions regarding the effective design of those controls. If a client’s management needed assistance in documenting their internal controls, Grant Thornton were willing to inform them of other available options. This decision would cost the firm millions of dollars in fees. It was a decision that left competitors rubbing their hands—a majority continued providing both services to clients. But then, people started coming out to affirm Grant Thornton in both their leadership and public position. That position was covered by Bloomberg, The New York Times and The Washington Post. The president and CEO of Financial Executives International (FEI) sent what she referred to as a “note of support,” which included her belief that Grant Thornton had now “set the bar for quality and independence.” |

Thought leadership coverage included Bloomberg, New York Times, Washington Post and Financial Executives International

|