Stock option expensing

|

Accounting rules said that the awarding of stock options to employees did not need to be reflected on the balance sheet of a company. Changes to this had been raised by the FASB in the 1990s, but was dropped. But it resurfaced again a decade later, driven in part by the high-tech boom where a majority of employee compensation was not in cash, but in stock options.

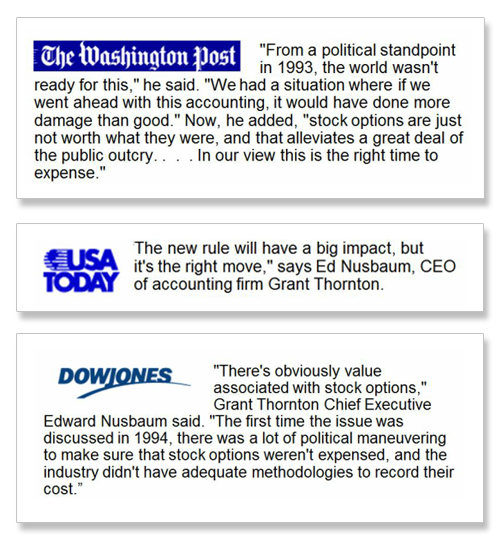

We were well-acquainted with both sides of the argument about putting these costs on the balance sheet. On the one hand, reliable measurement had been a valid concern. On the other hand, today’s tools are much more sophisticated (e.g., option-pricing models like Black-Scholes). than when the issue was last visited. It was time to rethink our position. Despite having more than 1,300 high-tech clients, bringing in nearly $100 million in revenues, we revised our opinion that stock options should be expensed and reflected on the balance sheet. This meant those same clients would have to account for a large amount of revenue and decrease earnings. We published a comment letter supporting FASB’s conclusions on Share-Based Payment, which said that stock options had to be reported as an expense. We were the first of the major accounting firms to take a public stand and state support for those conclusions. We activated our position with the press (coverage in many outlets including The Washington Post, USA Today and on the Dow Jones newswire) and influencers. This time, we also took our position to Capitol Hill, meeting with more than a dozen Senators and Representatives—in many cases facing strong disagreement. But, at the end of the day, we knew that we had done the right thing, bringing greater transparency to investors. |

|